Performance, Trends, Challenges & Opportunities

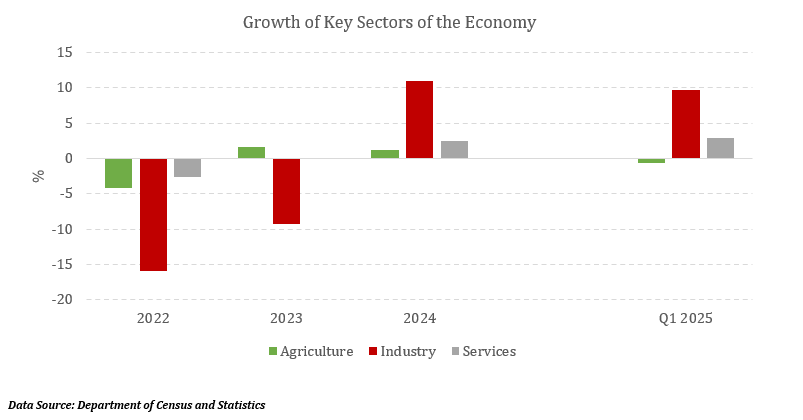

The industrial sector remains a critical pillar of Sri Lanka’s economy, contributing approximately 27% to GDP in 2024, with modest recovery following the deep contraction in 2022. The sector’s rebound is underpinned by easing monetary policy, stabilizing macroeconomic conditions, and a gradual recovery in domestic and external demand. Notably, manufacturing, especially food, beverages, textiles, and apparel, has shown resilience, despite global headwinds and domestic constraints.

Key Trends:

- Manufacturing Uptick: As of early 2025, manufacturing output expanded notably, driven by food & beverages, basic metals, and rubber/plastics. Apparel exports remain a key earner but face pressure from shifting global demand patterns and emerging trade barriers, especially in Western markets.

- Construction Recovery: Construction is showing tentative recovery with revived public infrastructure projects and easing credit conditions, although private investments remain subdued.

- Export Diversification: There is a visible policy and private sector push toward diversifying export portfolios, notably in value-added products, machinery, and chemical manufacturing.

Challenges:

- Energy Cost and Security: Geopolitical tensions (notably the US-Israel-Iran conflict) have heightened energy price volatility, increasing production costs for industries dependent on fossil fuels. Hedging and energy diversification remain limited.

- Labour Market Pressures: A persistent skills gap, particularly in advanced manufacturing, limits sectoral competitiveness, compounded by youth outmigration.

- Policy & Regulatory Bottlenecks: Protracted inefficiencies in trade facilitation, delays in port clearances, and slow adoption of the National Single Window continue to impede export-driven industries.

- External Trade Pressures: The recent imposition of reciprocal tariffs by the US, is expected to impact Sri Lanka’s industry sector, specifically the manufacturing sector. As global supply chains adjust, Sri Lankan exporters, especially in apparel, rubber-based products, and electronics components, face heightened competition and possible displacement effects. Furthermore, tighter US trade policy may dampen overall global demand, narrowing market access for Sri Lanka’s industrial exports.

Opportunities:

- Green Industrial Transformation: With Sri Lanka committed to scaling renewables to 70% of electricity generation by 2030, industries can leverage green energy, circular economy models, and sustainable manufacturing practices to improve cost efficiencies and align with global ESG standards.

- Digitalization: Industry 4.0 adoption remains nascent but presents vast potential in improving productivity, supply chain transparency, and market access, particularly for SMEs.

- Leveraging AI for Industrial Competitiveness: AI presents a transformative opportunity for Sri Lanka’s industry sector, particularly in enhancing productivity, operational efficiency, and product innovation. AI-driven solutions can optimize manufacturing processes through predictive maintenance, quality control automation, and supply chain optimization. Additionally, AI applications in data analytics can help industries better understand market trends and consumer preferences, positioning Sri Lankan manufacturers to compete in niche, high-value markets. Strategic investment in AI adoption, coupled with workforce upskilling, could elevate the global competitiveness of the country’s industrial base.

Outlook:

Sri Lanka’s industry sector is poised for moderate growth in 2025, supported by easing monetary conditions, a recovering domestic economy, and strategic reforms. The manufacturing sector, particularly apparel, food processing, and rubber-based industries, is expected to benefit from emerging opportunities in digitalization, AI adoption, and regional trade integration. However, risks remain elevated with rising US trade protectionism, geopolitical-driven energy price volatility, and persistent structural constraints such as skills shortages and regulatory inefficiencies. The pace of recovery will hinge on the industry’s ability to diversify export markets, invest in sustainable and green manufacturing practices, and harness technological innovations to drive competitiveness in a challenging global environment.